Published on

- 4 min read

Your Thirties: The Decisive Decade for Building Wealth

Your thirties are not just another phase of life. For most people, it is the single most financially transformative decade they will ever experience. The choices you make — or fail to make — between ages 30 and 40 will shape your retirement readiness, your kids’ college options, your ability to take risks, and your overall quality of life for decades to come.

Why your thirties specifically? Because it is the decade where several powerful forces converge: your earning power is at its highest growth trajectory, your expenses have stabilized, you have enough career experience to command real salary, and time is still on your side — compound interest still has decades to work its magic.

But here is the uncomfortable truth: the median retirement savings for Americans in their thirties sits at roughly $30,000, according to Federal Reserve data. That figure is not enough. Not even close. If you are starting at zero or close to it, do not panic — but do not wait, either.

The Income Jump Most People Miss

The single biggest financial opportunity in your thirties is not investment returns — it is career earnings growth. Research from the Federal Reserve Bank of New York shows that median earnings for workers in their thirties increase by roughly 50% to 70% between ages 30 and 40 in most industries. That is not a small bump — that is a life-altering shift in your financial capacity.

Most people, however, treat their thirties like their twenties. They maintain the same lifestyle. They upgrade the same things — nicer apartment, newer car, more dining out — as their income rises. This is what researchers call lifestyle creep, and it is the silent wealth killer.

The alternative: bank the raise. When your income increases by $10,000 a year, allocate at least $7,000 of that to savings and investments. Live on the remaining $3,000 upgrade. You still get to enjoy more — but you also build real wealth.

The Retirement Window Is Closing

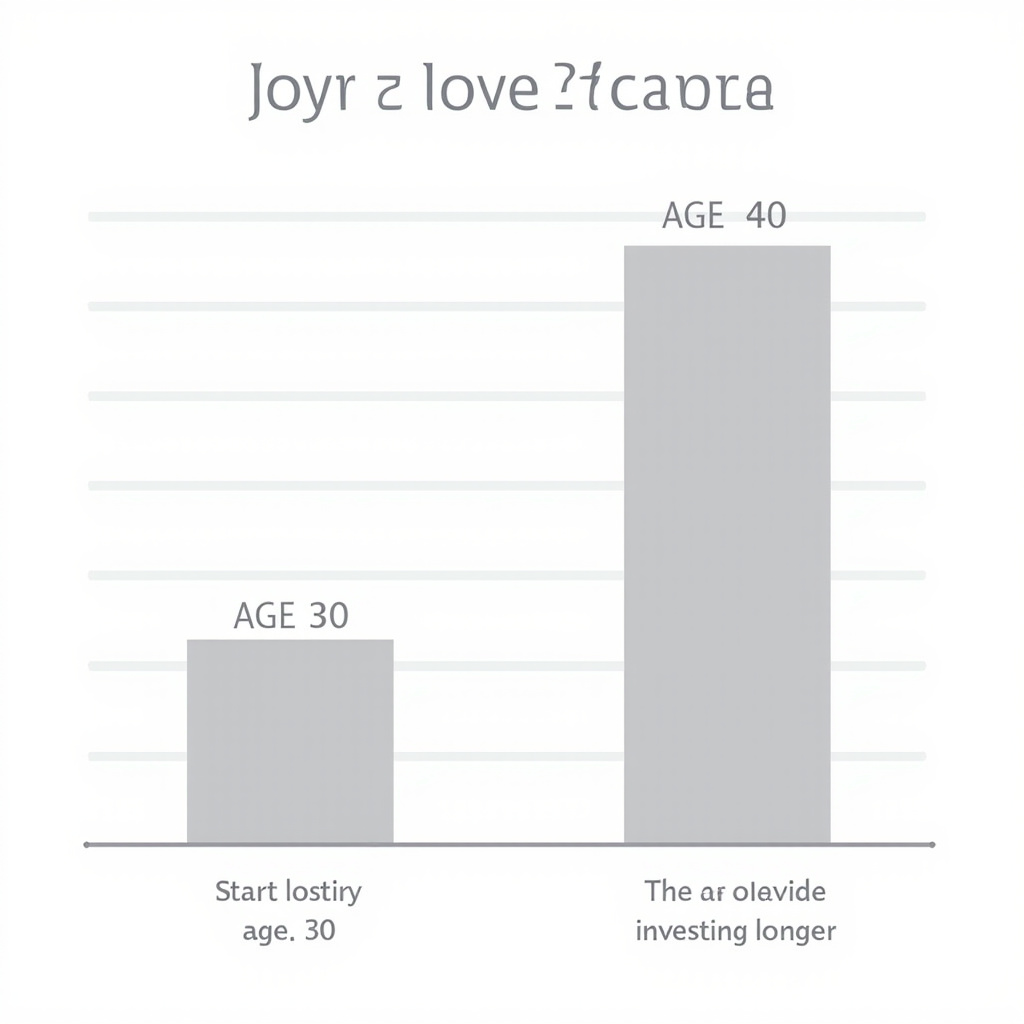

The math of retirement savings is brutally time-sensitive. A 30-year-old who invests $500 per month at an average 7% annual return will have approximately $604,000 by age 60. A 40-year-old doing the same thing will have only $244,000. Same contribution, same return, less than half the result — all because of the lost decade of compounding.

If your employer offers a 401(k) match, contribute enough to get the full match. That is free money. Then increase your contribution rate by 1% every year until you reach at least 15% of your gross income. Automate the increase so you never have to think about it.

The Debt Decision

Your thirties are also the decade where debt can either build your future or destroy it. Good debt — a mortgage on a reasonable home, student loans that enabled a career — can be manageable. Bad debt — credit card balances, car loans on depreciating assets, personal loans for lifestyle spending — will compound against you.

If you enter your thirties with consumer debt, make eliminating it your top financial priority. The interest you pay on a $5,000 credit card balance at 24% APR is money that could be growing in your retirement account instead.

Invest Aggressively While You Can

In your thirties, you have the one thing older investors do not: time to recover from market downturns. This means you can and should invest more aggressively. A portfolio heavily weighted toward low-cost index funds — domestic and international — is the optimal strategy for most people in this age range.

Do not try to pick stocks. Do not chase trends. Do not time the market. Invest consistently, diversify broadly, and let compounding do the work.

The Three Moves That Matter Most

- Maximize your earning potential. Negotiate your salary, change jobs strategically, develop skills that increase your market value.

- Automate your savings. Set up automatic contributions to retirement accounts, emergency funds, and investment accounts. Remove the decision from your daily life.

- Avoid lifestyle creep. For every dollar your income increases, save at least 70 cents.

The Bottom Line

Your thirties are not a rehearsal. They are the main event. The financial habits you build now — good or bad — will compound for the next 30 to 40 years. You do not need to be perfect. You need to be intentional. Start where you are, use the strategies above, and let time do the heavy lifting. A decade from now, you will be grateful you started today.

Related Articles

The 50/30/20 Budget Rule: Your Simple Blueprint for Financial Freedom

Learn the simple 50/30/20 budgeting method that helps you allocate your income wisely without compli...

Why Your Savings Account is Costing You Money

Discover why keeping all your money in a traditional savings account might be silently eroding your ...

Compound Interest: The Most Powerful Force in Finance

Discover why Einstein called compound interest the eighth wonder of the world and how to harness its...