Published on

- 4 min read

Debt Snowball vs. Debt Avalanche: Which Strategy Wins?

You have multiple debts. You have a fixed amount of extra money each month to put toward them. The question is: which debt do you tackle first?

Two popular methods — the debt snowball and the debt avalanche — take very different approaches to that answer. Here is how they work, and which one is actually better for your situation.

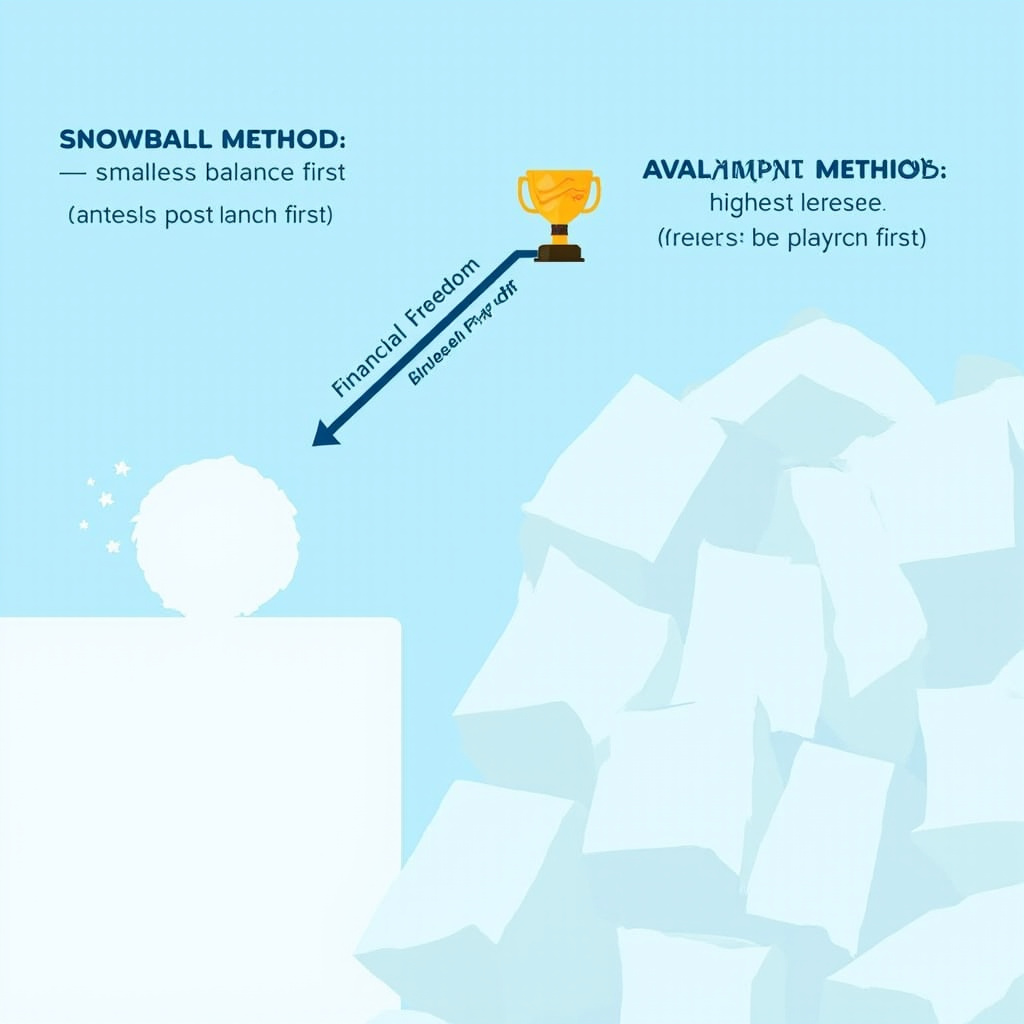

The Two Methods

Debt Snowball, popularized by personal finance author Dave Ramsey, focuses on your smallest balance first. You make minimum payments on everything else, throw all extra money at the smallest debt, and once it is paid off, you move to the next smallest. It is like rolling a snowball downhill — each win builds momentum.

Debt Avalanche, the mathematically optimal approach, targets the highest interest rate first. Same process otherwise: minimum payments on everything, all extra cash toward the debt with the highest rate, then roll that payment into the next highest-rate debt as each one clears.

A Practical Example

Say you have three debts, using real data:

| Debt | Balance | APR | Minimum Payment |

|---|---|---|---|

| Credit Card A | $3,260 | 22% | $130 |

| Credit Card B | $5,500 | 24% | $200 |

| Student Loan | $38,000 | 7.5% | $410 |

The credit card balances reflect real 2023 U.S. averages by age group (Statista). The student loan figure is the national per-borrower average as of 2024 (Federal Reserve and Education Department data). Interest rates reflect the actual range: average credit card APR hit 24.37% in January 2025 (Investopedia), while federal student loans ran 6.53% to 9.08% in 2024.

With the snowball, you attack the $3,260 credit card first (smallest balance). Once paid off, you roll its $130 minimum into the $5,500 card, giving you $330 a month to accelerate that payment. After both credit cards are gone, you combine both minimums — $530 a month — toward the student loan. Quick win, psychological momentum.

With the avalanche, you attack the $5,500 credit card first (24% APR, the most expensive debt). Same roll-over mechanics apply. You free up $200 after that card clears, pour it into the $3,260 card, then attack the student loan. The math is straightforward: 24% compounding against you is far more expensive than 7.5%.

The Psychology Factor

Mathematically, the avalanche is the clear winner. If both methods are followed completely, the avalanche will always cost you less in total interest paid.

But here is what the numbers do not capture: behavior matters. The debt snowball is designed around momentum. Getting that first small debt to zero, quickly, creates a psychological win that encourages people to keep going. For many people drowning in debt, the avalanche can feel like an eternity before seeing any result — and that leads to giving up.

Research from James Madison University found that while the avalanche minimizes total interest paid, the snowball’s psychological advantage means people are more likely to stay committed to the payoff plan long enough to actually finish. And finishing is what matters most.

When Each Method Makes Sense

Choose the Snowball if:

- You are new to debt payoff and need early wins to stay motivated

- Your debts are all roughly similar in size

- You have already struggled with debt payoff attempts in the past

- You are the type who needs visible progress to stay on track

Choose the Avalanche if:

- You are disciplined and can stay focused without frequent validation

- You have a large high-interest debt that is costing you serious money

- You want to minimize the total interest you pay over the life of the payoff

- You are driven more by numbers than feelings

What About the Third Option?

The worst option — and the most common one — is making no plan at all. If you are just paying minimums on everything and not directing extra money anywhere strategic, you are paying the maximum possible in interest over the longest possible timeline. Either method above will beat that approach.

The Honest Truth

The best debt payoff strategy is the one you will actually follow. If the avalanche’s longer timeline without early wins makes you want to quit, it does not matter that it would save you $500 in interest — because you will not finish. Conversely, if the snowball’s quick wins get you excited and you end up debt-free faster as a result, the slightly higher interest cost is well worth it.

But if you have the discipline to stick with a plan that does not give you early gratification, and you are carrying high-interest credit card debt that is genuinely expensive, the avalanche is the smarter choice.

Start Today

Whatever method you choose, the starting point is the same:

- List every debt with its balance, interest rate, and minimum payment

- Calculate how much extra you can put toward debt each month after covering the essentials

- Pick your method, commit to it, and begin

The biggest mistake people make is waiting until their finances are perfect to start. They never are. Start now.

Related Articles

The 50/30/20 Budget Rule: Your Simple Blueprint for Financial Freedom

Learn the simple 50/30/20 budgeting method that helps you allocate your income wisely without compli...

6 Costly Money Mistakes Most Americans Make

Learn about the six most common and expensive financial mistakes that keep Americans broke, and how ...

How to Save $1,000 a Month: A Realistic Guide

A practical, step-by-step guide to saving $1,000 per month without extreme frugality or sacrificing ...