Published on

- 4 min read

Emergency Fund: Your First Financial Priority

Imagine losing your job tomorrow. How long could you keep paying your bills without touching your investments or racking up credit card debt? If that number is measured in weeks rather than months, you are not as financially secure as you think — and you are definitely not alone.

An emergency fund is money set aside specifically to cover unexpected expenses or a loss of income. It is not an investment. It is not for vacations or a new phone. It is your financial safety net — and it is the foundation every sound financial plan starts with.

Why You Need One

The Federal Reserve 2024 Survey of Household Economics and Decision-Making found that 63% of American adults could cover an unexpected expense using cash or cash equivalents. That sounds reassuring — until you consider the other side of the data: 59% of Americans in 2025 do not have enough savings to cover a $1,000 emergency expense, according to Bankrate’s annual emergency savings report.

Without an emergency fund, you have two options when trouble hits: put it on a credit card carrying 15 to 25% interest, or liquidate investments at the worst possible time. Neither is good. A solid emergency fund means you never have to make that choice.

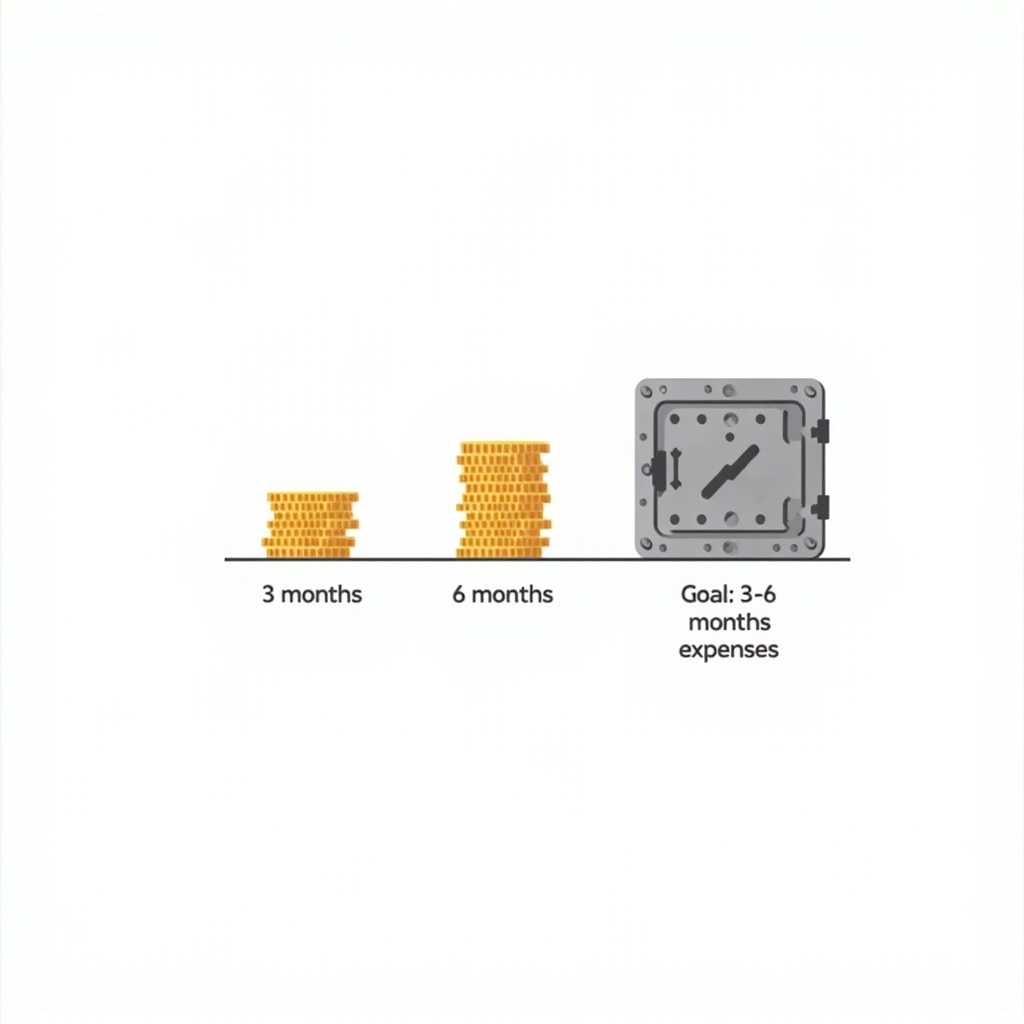

How Much Is Enough?

The standard recommendation is three to six months of essential living expenses. “Essential” is the key word. We are talking rent or mortgage, utilities, groceries, health insurance, car payments, and minimum debt payments. Not dining out, subscriptions, or discretionary spending.

- Three months may be sufficient if your job is very stable.

- Six months is the baseline for most people.

- Six to twelve months makes sense if you are self-employed, work on commission, have a single income in the household, or have dependents relying on you.

A four-person American family should plan for roughly $33,000 to cover six months of essential expenses, based on cost estimates: healthcare and insurance $10,754, car costs $10,250, housing and utilities $9,137, and groceries $2,969. That number is sobering — and it underscores why building this fund is a process, not an overnight switch.

Where to Keep It

An emergency fund must be liquid, safe, and separate from your everyday spending account. A high-yield savings account (HYSA) is the right home for this money.

As of early 2025, the best HYSA rates are around 4.5% to 4.75% APY — more than 11 times the national average of 0.41% for regular savings accounts. Online banks like Ally, Marcus by Goldman Sachs, and Vio Bank consistently top the HYSA rankings. The money is FDIC-insured up to $250,000.

Do not put your emergency fund in stocks, bonds, ETFs, or cryptocurrency. You need this money available the moment you need it — not waiting for the market to recover.

How to Build It

Start with a small, achievable milestone. Aim for $1,000 to $2,000 as your first mini-goal. That alone covers most minor emergencies and prevents you from reaching for a credit card immediately.

- Calculate your monthly essentials

- Set your target (3–6 months of that number)

- Automate it — set up a recurring transfer from your checking account to your emergency HYSA the day after each paycheck lands

- Protect it — if you dip into it, rebuild it as your first priority before anything else

The 50/30/20 budget framework is a useful guide here: your 20% savings allocation should first fill your emergency fund before any other financial goals get a dollar.

The Bottom Line

An emergency fund is not exciting. It will not double your net worth or get you to retirement faster. But it is the thing that stands between you and financial disaster when life goes sideways — and life always goes sideways at some point.

The good news: this is one of the most actionable financial goals you can set. You do not need a high income to start. You need consistency and a separate account. Open a HYSA today, set a small automatic transfer, and start building. Three months from now, you will be in a fundamentally different position than you are today — and that peace of mind is worth more than any interest rate.

Related Articles

The 50/30/20 Budget Rule: Your Simple Blueprint for Financial Freedom

Learn the simple 50/30/20 budgeting method that helps you allocate your income wisely without compli...

Why Your Savings Account is Costing You Money

Discover why keeping all your money in a traditional savings account might be silently eroding your ...

6 Costly Money Mistakes Most Americans Make

Learn about the six most common and expensive financial mistakes that keep Americans broke, and how ...