Published on

- 4 min read

How to Build Credit from Scratch

You have just moved to a new country, you are a student, or you have simply never borrowed money before. Either way, you have no credit history and no credit score. That might sound like a good thing. But in the United States, no credit history is not neutral — it is invisible. And when you are invisible to the financial system, landlords ask for six months upfront, car loans come with punishing interest rates, and some employers even check your credit before hiring.

Building credit from scratch is one of the most important early steps in your financial life. The good news: it is simpler than most people think, and it does not take as long as you might expect.

How Credit Scores Actually Work

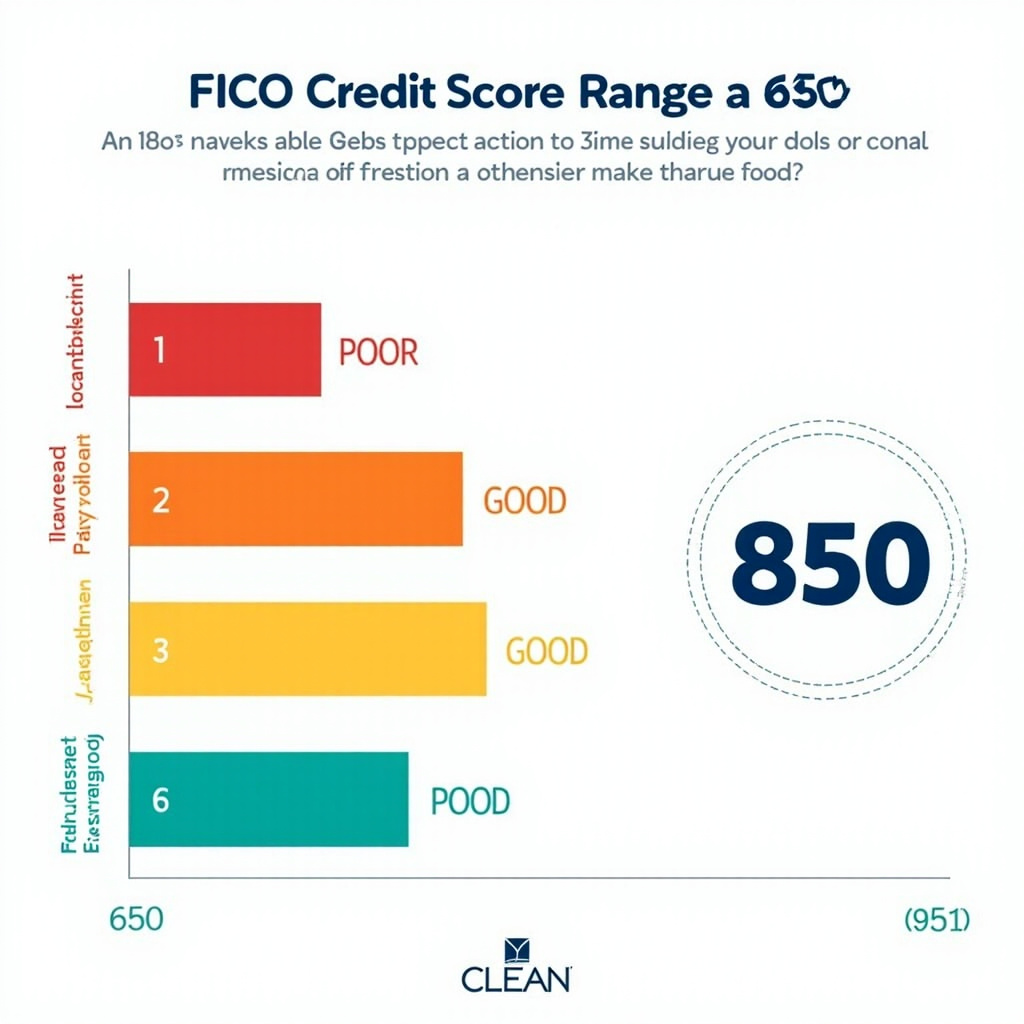

Most credit scores in the United States are calculated using the FICO model, developed by the Fair Isaac Corporation. Scores range from 300 to 850, with higher numbers representing better creditworthiness. Three major credit bureaus — Equifax, Experian, and TransUnion — compile your credit reports, and FICO uses those reports to generate your score.

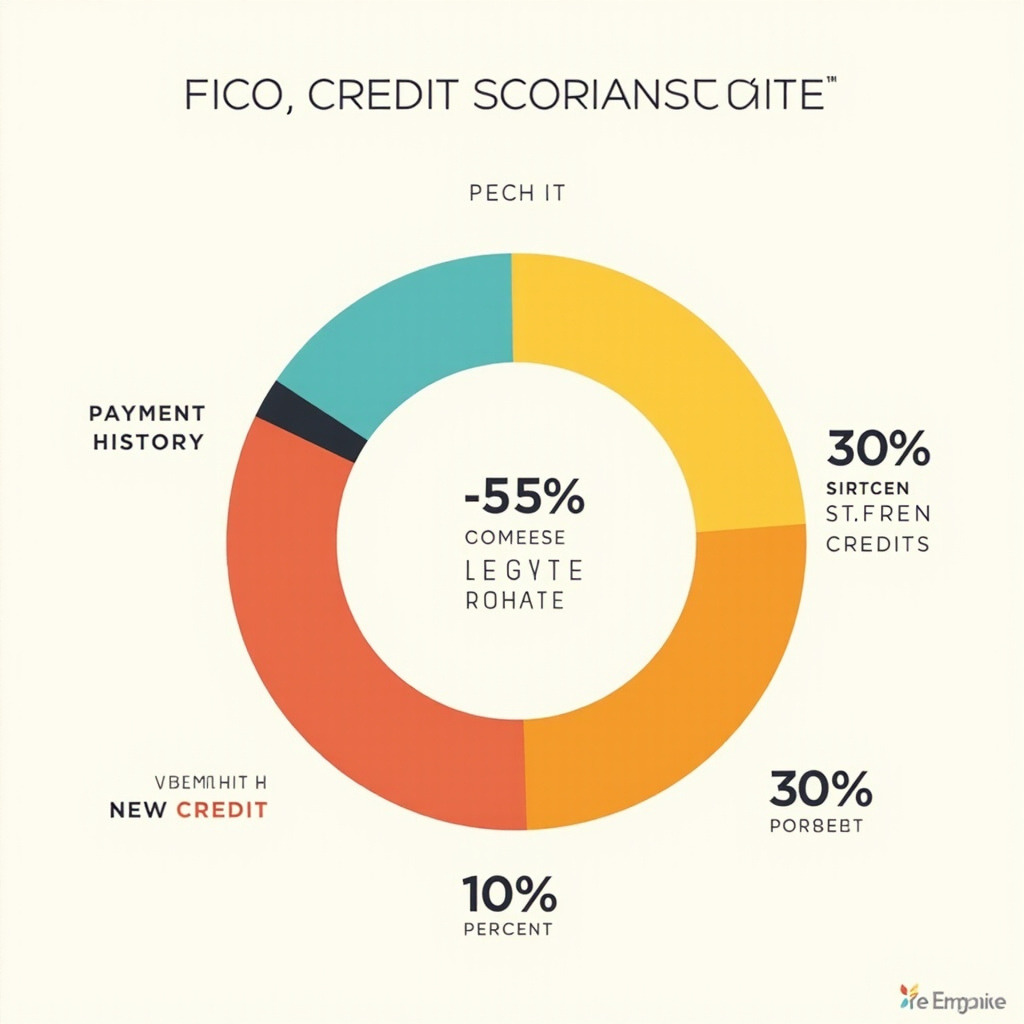

Five factors determine your score:

- Payment history (~35% of your score)

- Amounts owed relative to credit limits (~30%)

- Length of credit history (~15%)

- New credit (~10%)

- Credit mix (~10%)

The most important takeaway: payment history is by far the biggest single factor. Paying your bills on time, every time, is the foundation everything else is built on.

Step 1: Check Your Starting Point

Before you build anything, you need to know where you stand. You are entitled to a free copy of your credit report from each of the three major bureaus once every 12 months at AnnualCreditReport.com. Check all three reports carefully for errors. Incorrect information, such as accounts that do not belong to you or payments incorrectly marked late, can drag down a score you are trying to build.

Step 2: Become an Authorized User

This is the single fastest way to establish a credit history. Ask a family member or trusted friend with a credit card in good standing to add you as an authorized user. You do not need to use the card — or even have a copy of it. The account’s payment history gets reported to your credit file, giving you an instant track record.

Not all card issuers report authorized user activity to all three bureaus, so confirm this before proceeding. When it works, it is the closest thing to a shortcut in the credit-building world.

Step 3: Apply for a Starter Credit Card

If being an authorized user is not an option, your next move is a secured credit card. These cards require a cash deposit — typically $200 to $500 — which becomes your credit limit. Because the deposit eliminates the lender’s risk, approval is nearly guaranteed even with no credit history.

Use the card for small, regular purchases — a streaming subscription, groceries, or gas — and pay the balance in full every month. The goal is not to spend money. It is to generate a consistent pattern of on-time payments.

Step 4: Pay Every Bill on Time

This cannot be overstated. A single missed payment can stay on your credit report for up to seven years and drop your score by 60 to 110 points. Set up automatic payments for at least the minimum due on every account. If you are worried about overdrafts, set calendar reminders and pay manually — but never miss a due date.

Step 5: Keep Your Utilization Low

Credit utilization — the percentage of your available credit that you are actually using — accounts for roughly 30% of your score. The rule of thumb: stay below 30% utilization, and ideally below 10%. On a $500 secured card, that means keeping your balance under $150 — and ideally under $50.

Step 6: Be Patient and Monitor Your Progress

Credit building is a marathon, not a sprint. Most people can achieve a score of 670 or higher (considered “good” by most lenders) within 6 to 12 months of responsible credit use. Check your score regularly through free services like Credit Karma or your card issuer’s app, but do not obsess over daily fluctuations.

The Bottom Line

Building credit from scratch is not complicated. It requires three things: a credit account in your name, consistent on-time payments, and patience. Start with a secured card or authorized user status, keep your balances low, and let time do the rest. Six months from now, you will have a score. A year from now, you will have options. And that is worth far more than any shortcut.

Related Articles

The 50/30/20 Budget Rule: Your Simple Blueprint for Financial Freedom

Learn the simple 50/30/20 budgeting method that helps you allocate your income wisely without compli...

6 Costly Money Mistakes Most Americans Make

Learn about the six most common and expensive financial mistakes that keep Americans broke, and how ...

Credit Score Basics: What You Need to Know

Everything you need to understand about credit scores — how they work, why they matter, and how to i...