Published on

- 3 min read

The Hidden Cost of Lifestyle Inflation: Why Your Raise Disappears

You worked hard, got promoted, and finally got that long-awaited salary bump. A 10% increase — congratulations! You should be richer now, right?

So why does your bank account look exactly the same?

Welcome to the silent killer that financial planners call lifestyle inflation, and it is quietly taking raises from millions of Americans before they ever hit their savings account.

It Feels Like a Raise, But It Is Not

The mechanism is almost invisible. Your income goes up, and so does your standard of living. New car. Bigger apartment. Dining out more often. A vacation you could not afford last year.

The math is simple and brutal: if your spending grows at the same rate as your income, you are not actually getting wealthier. You are just running faster on the same treadmill.

What the Data Shows

Despite years of financial advice urging workers to build savings after pay increases, survey data consistently shows that most Americans do not meaningfully increase their savings rate after getting a raise. Studies tracking household financial behavior find that spending increases tend to match or closely track income increases for most workers, regardless of income level.

Where did the raise go? Lifestyle upgrades.

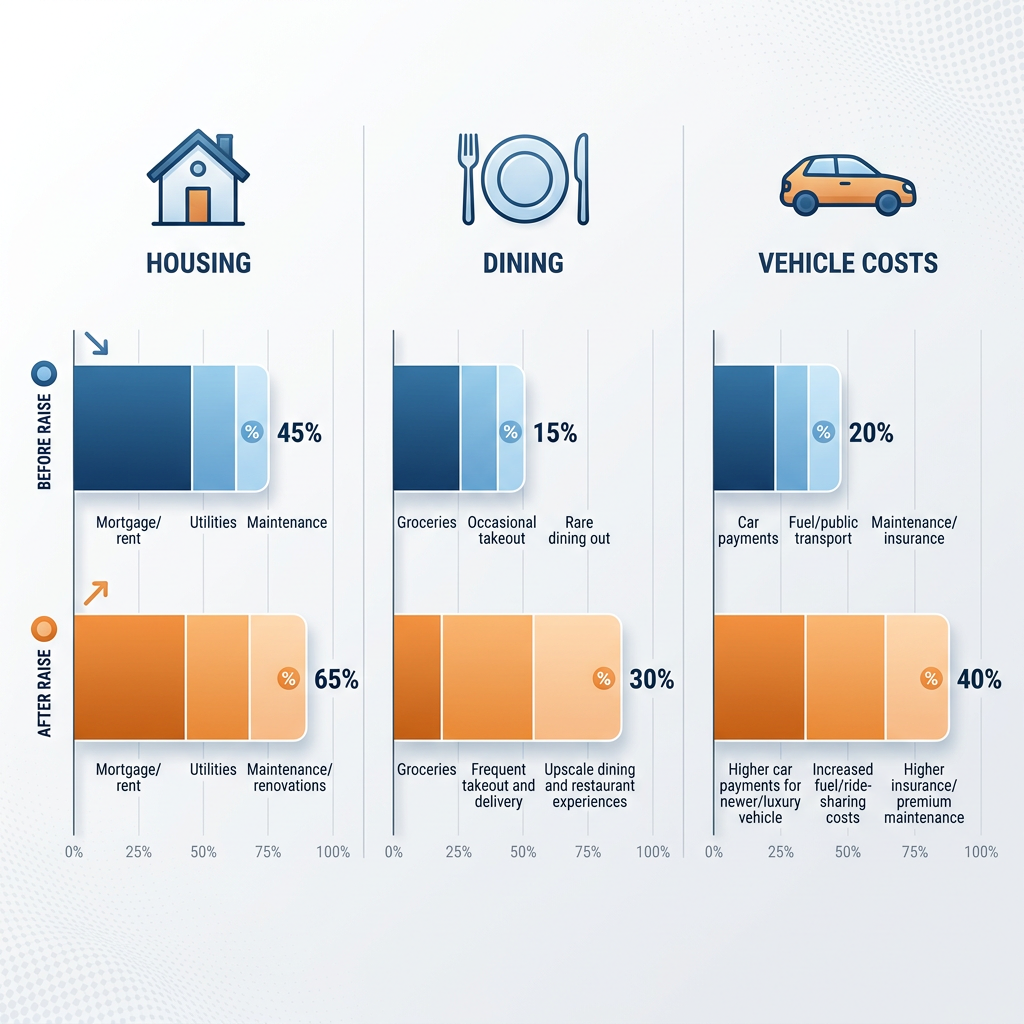

Research tracking spending patterns finds that housing costs tend to rise significantly after income increases, dining expenses tend to increase, and vehicle purchases shift from used to new models within two years of a meaningful raise. The new lifestyle feels normal within months, and the previous baseline no longer feels adequate.

The Psychology Behind It

Behavioral economists have a name for why this happens: hedonic adaptation. Humans are remarkably good at adjusting to new circumstances — both good and bad. When you get a raise, the initial thrill of financial relief fades within months. The new salary becomes the baseline, and the previous lifestyle no longer feels satisfying.

You upgrade, and then the upgrade becomes normal. Then you upgrade again. The cycle never ends because the satisfaction never lasts.

How to Break the Cycle

- Bank the raise before you feel it. When your income increases, automatically direct at least 50% of the increase to savings and investments before you adjust your lifestyle. If you never see it in your checking account, you will not miss it.

- Set a lifestyle ceiling. Decide in advance what your ideal annual spending level is — and do not exceed it regardless of income growth. All income above that ceiling goes to building wealth.

- Wait 90 days before any major upgrade. When you feel the urge to upgrade your car, apartment, or wardrobe, wait 90 days. Most urges pass. The ones that remain are usually worth acting on.

- Track your savings rate, not your income. Income is vanity. Savings rate is reality. If your savings rate is not increasing as your income grows, you are not making progress.

The Bottom Line

Lifestyle inflation is not a character flaw. It is a human tendency that affects nearly everyone who earns more money. The difference between those who build wealth and those who do not is not income — it is the ability to resist the urge to upgrade every time a raise arrives.

The next time you get a raise, celebrate. Then automate the savings. Your future self will thank you.

Related Articles

The 50/30/20 Budget Rule: Your Simple Blueprint for Financial Freedom

Learn the simple 50/30/20 budgeting method that helps you allocate your income wisely without compli...

6 Costly Money Mistakes Most Americans Make

Learn about the six most common and expensive financial mistakes that keep Americans broke, and how ...

How to Save $1,000 a Month: A Realistic Guide

A practical, step-by-step guide to saving $1,000 per month without extreme frugality or sacrificing ...