Published on

- 4 min read

How to Save Money on Health Insurance in 2026 — Without Sacrificing Coverage

Every working American knows the feeling: opening the email or letter that lists the new health insurance premium, watching the number climb yet again, and wondering how the cost of a piece of paper that promises to pay your medical bills has outpaced both wages and inflation for two decades running.

Health insurance in 2026 remains one of the largest recurring expenses for most households, and one of the most confusing. But the system is not as inscrutable as the insurance industry would like you to believe. Most households are leaving meaningful money on the table every year — not because the insurance is fundamentally unaffordable, but because they are not using the tools and strategies that exist to reduce the cost.

How Health Insurance Pricing Works in 2026

To save money on health insurance, you first need to understand what you are actually paying for.

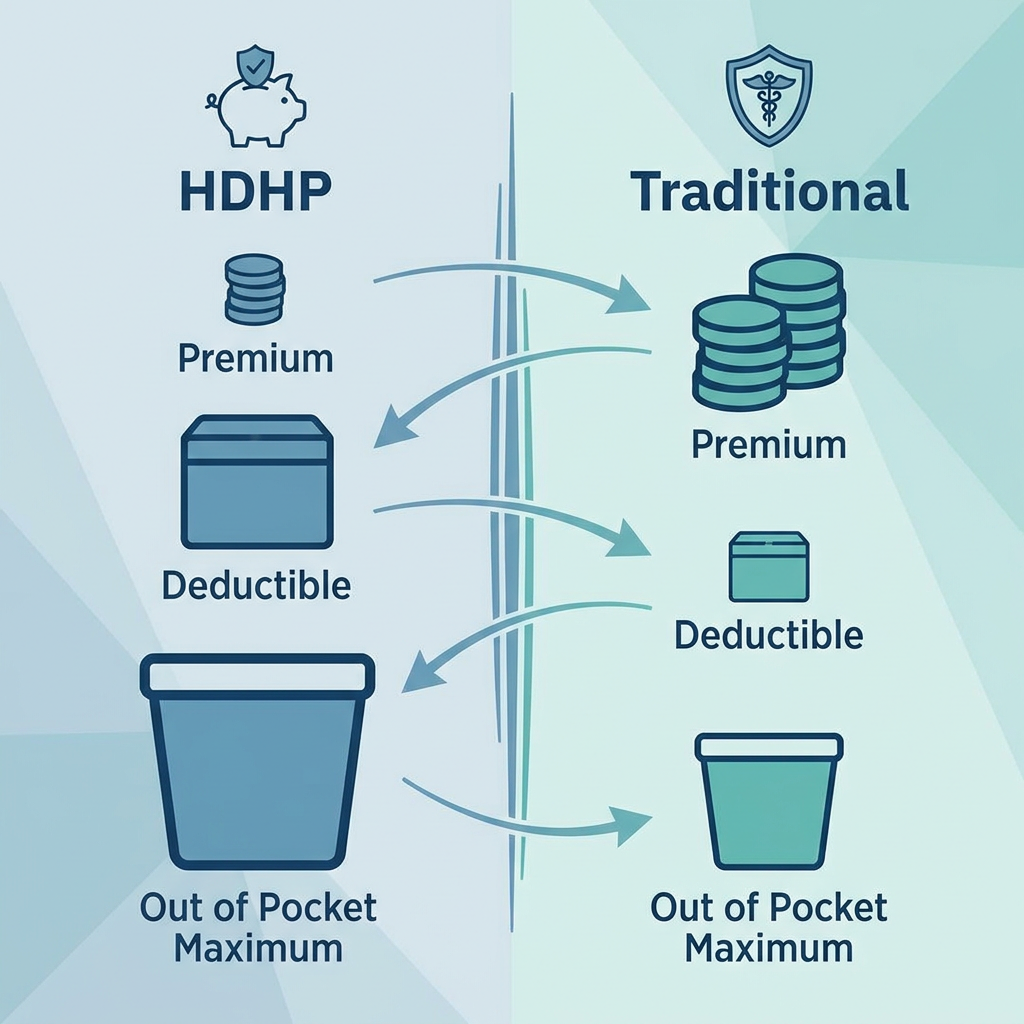

The premium is the monthly amount you pay to keep coverage active. Premiums for employer-sponsored family coverage now routinely exceed $24,000 per year, with the employee typically paying 25% to 30% of that.

The deductible is the amount you pay out of pocket for covered services before insurance starts paying. In 2026, deductibles for employer plans commonly range from $1,500 to $3,000 for individuals.

The out-of-pocket maximum is the most important number most consumers never look at — it is the absolute ceiling on what you will pay in a year for covered services, excluding premiums. Knowing this number, and choosing a plan with a manageable maximum relative to your savings, is the single most important financial decision in health insurance.

The HDHP-HSA Strategy: Best for Many Households

For households with stable employment, predictable medical needs, and the financial discipline to save, the combination of a High Deductible Health Plan (HDHP) and a Health Savings Account (HSA) is almost always the most cost-effective option.

Here is why: HDHPs have lower premiums — often $200 to $400 per month less than traditional plans. The money you save on premiums goes into an HSA, which offers a triple tax advantage: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free.

In 2026, the HSA contribution limits are $4,300 for individuals and $8,550 for families, with an additional $1,000 catch-up contribution for those 55 and older. Over time, an HSA can grow into a significant retirement asset — the only account in the American tax system that is triple tax-advantaged.

Subsidies and Marketplace Options

If you do not have employer-sponsored insurance, the Affordable Care Act marketplace may offer significant savings. Subsidies are available for households earning between 138% and 400% of the federal poverty level, and many households at the lower end of that range pay less than $100 per month for comprehensive coverage.

The key is to actually shop during open enrollment. Many eligible households never check the marketplace because they assume the plans are too expensive or the process is too complicated. In 2026, the enrollment process has been streamlined significantly, and subsidy calculators make it easy to estimate your costs before you apply.

Negotiating Medical Bills

Even with insurance, medical bills can be staggering. The single most effective strategy for reducing out-of-pocket costs is negotiation. Hospitals and providers routinely accept reduced payments from insured patients who ask.

Request an itemized bill and review it for errors — duplicate charges, incorrect codes, and services you did not receive are common. Then call the billing department and ask for a discount or payment plan. Many hospitals offer financial assistance programs that can reduce or eliminate bills for households below certain income thresholds.

Preventive Care Is Free — Use It

Under the ACA, all marketplace and employer plans must cover preventive services at no cost — no copay, no deductible. This includes annual physicals, screenings for cancer, diabetes, and heart disease, immunizations, and well-woman visits.

Most Americans do not use all the preventive services available to them. A routine screening that catches a condition early can save thousands in treatment costs later. Preventive care is not just good health practice — it is good financial practice.

The Bottom Line

Health insurance in 2026 is expensive, but it is not immutable. The HDHP-HSA strategy can save thousands for disciplined households. Marketplace subsidies can dramatically reduce costs for eligible families. Negotiation and preventive care can further reduce out-of-pocket expenses.

The households that save the most are the ones that treat health insurance as a financial decision, not just a benefit. Shop during open enrollment. Compare plans. Maximize your HSA. Negotiate bills. Use preventive care. The savings are real, and they compound over time.

Related Articles

The 50/30/20 Budget Rule: Your Simple Blueprint for Financial Freedom

Learn the simple 50/30/20 budgeting method that helps you allocate your income wisely without compli...

6 Costly Money Mistakes Most Americans Make

Learn about the six most common and expensive financial mistakes that keep Americans broke, and how ...

How to Save $1,000 a Month: A Realistic Guide

A practical, step-by-step guide to saving $1,000 per month without extreme frugality or sacrificing ...